Showing posts with label Becoming an Investment Banker. Show all posts

Showing posts with label Becoming an Investment Banker. Show all posts

Monday, August 01, 2011

Untangling the Ropes of Investment Banking in Corporate Setting

Thursday, August 26, 2010

Investment Banking Career Advice: Where to Get It?

From what I could learn through the website, the company offers connections to investment banking executives for career advice, job search help, interview prep, etc. Seemed interesting, but I wanted to find out more, so I reached out to the guy who runs the site to find out more. It turns out that the site’s founder, Chris Carey, is a young guy who used to work as an investment banking analyst, and he was able to put me in touch with a recent customer of his company.

He connected me to Matt, a 25-year old former hedge fund analyst that is hoping to snag an M&A or Equity Research position at a bulge-bracket investment bank in New York. You can read what Matt wrote me about Blue Chip Career below:

Investment Banking Monkey: Why did you decide to try Blue Chip Career?

After a few false starts on Wall Street due to the recession and bad luck, I found myself with an incoherent resume and having not gotten the bulge-bracket experience I have long sought. In searching for investment banking career counselors, I came across Blue Chip Career. Because Chris runs a third-party service, Blue Chip Career can tailor your consultations according to your needs and objectives. You aren’t talking to a solo practitioner who might claim their expertise is well-rounded when it is not. With Blue Chip Career, Chris has brought together a group of advisors with experience in every corner of Wall Street.

Which advisors did you speak with?

I met with three advisors, Patrice Green, Ozgur Demirial, and Pierre (PJ). I chose these advisors, because they had backgrounds at both bulge bracket investment banks and hedge funds.

What was the consultation experience like with these advisors?

I saw PJ first, and we met at a Starbucks. Because he is launching a hedge fund and will be looking to hire, PJ has the perspective of a potential employer. For example, when I mentioned that I am planning to get an MBA in a few years, he immediately cut me off and said he would be more likely to hire me if I have a CFA, and that is a sign of things to come on Wall Street. His straightforwardness and experience in both Equity Research and Investment Banking combine for a well-rounded perspective. Additionally, he was quick to point out a few kinks and inconsistencies in my resume.

I met Ozgur a week later. As a CFA who has worked in both Investment Banking and Hedge Funds, he has a different perspective from many on Wall Street who say that the CFA does not provide many marketable skills within the investment banking sector. As he is now working in Asset Management/Hedge Funds, that constituted the bulk of our conversation. He immediately jumped on my resume as soon as I handed it to him, pointing out a few things that could be revised.

My last meeting was with Patrice. She had worked under a few of the most powerful people in Wall Street history, so as we discussed the history of Wall Street since the 1980’s she gave me a very interesting perspective on the evolution of the investment banking business. As she runs a fund, she was very up to date with the employment market and what bulge bracket firms are really looking for. She also reminded me that getting a job involves a great amount of politics, as does advancing within a firm once you are working there. As PJ and Ozgur did, she gave me a number of pointers on my resume.

Would you recommend this service to a friend? If so, why?

Absolutely. It can be scheduled at your convenience, a very customer-is-right feature. It is geared toward people my age whose career path may have been thrown off by the recession, and the advice is from people who have years of high-level experience on Wall Street.

I was definitely hesitant at first to pay for career advice, but I’m glad that I decided to schedule my consultations, as they were a great help and value to my career. In fact, I plan on using Blue Chip Career again as my career progresses.

Sunday, January 24, 2010

Extending Your Investment Banking Network

If you have graduated from a reputable university, going to investment banking will be easier for you. Getting a banking interview is not hard. However there are some that might have a hard time because the process is not simple. You need to be active so that there is no need for recruiters to schedule you. Build a network that you can rely on in the future. It is good to start to have friends and acquaintances that can schedule you for interview. Use your former classmates because there are few of them that might actually be in the financial industry.

Friday, July 20, 2007

...and the kind of shit that (often) happens in investment banking

... continued from "The kind of shit that (not so often) happens in investment banking"

You waltz into the office at around 10:30 am, feeling like you own the place in light of the information you acquired the night before, on your way home from work. You get to your desk, drop your things onto loudly, look at your phone, where the red indicator light is blinking indicating that you have voicemails, and choose to ignore it. You pick up the phone to Mike, one of your buddies in the industrial manufacturing group and arrange to meet him at the lifts for coffee. You take a stroll around the floor, saying hi to fellow monkeys and the secretaries, and stopping by to exchange a few (condescending, given that you are now a pro forma master of the universe) words with each of them.

"Don't you have work to do man?"

Asks one of the summer interns, who is religiously compiling annual and quarterly reports for the comps he needs to do.

"My man, you will learn. In time, you will learn... not to ask silly questions like that"

As you pass more and more people in the office, blatantly demonstrating the fact that you are really doing nothing, more heads start to turn, and you can hear the puzzled whispers as you pass each desk.

"Is he quitting?"

You barely make out the words coming from behind you, as you make your way to the lifts.

You chuckle, as you make out the words. Little do they know what is really on the table, you think to yourself and picture yourself turning around, walking over the the little naive monkey who asked the question and saying:

"Little man, quitting is for amateurs. For the guys that aren't good enough to stay. I am by no means quitting. Mark these words, as you are talking to the future department head... and when you know the kind of shit that I know, that won't be in the too distant future".

You waltz into the office at around 10:30 am, feeling like you own the place in light of the information you acquired the night before, on your way home from work. You get to your desk, drop your things onto loudly, look at your phone, where the red indicator light is blinking indicating that you have voicemails, and choose to ignore it. You pick up the phone to Mike, one of your buddies in the industrial manufacturing group and arrange to meet him at the lifts for coffee. You take a stroll around the floor, saying hi to fellow monkeys and the secretaries, and stopping by to exchange a few (condescending, given that you are now a pro forma master of the universe) words with each of them.

"Don't you have work to do man?"

Asks one of the summer interns, who is religiously compiling annual and quarterly reports for the comps he needs to do.

"My man, you will learn. In time, you will learn... not to ask silly questions like that"

As you pass more and more people in the office, blatantly demonstrating the fact that you are really doing nothing, more heads start to turn, and you can hear the puzzled whispers as you pass each desk.

"Is he quitting?"

You barely make out the words coming from behind you, as you make your way to the lifts.

You chuckle, as you make out the words. Little do they know what is really on the table, you think to yourself and picture yourself turning around, walking over the the little naive monkey who asked the question and saying:

"Little man, quitting is for amateurs. For the guys that aren't good enough to stay. I am by no means quitting. Mark these words, as you are talking to the future department head... and when you know the kind of shit that I know, that won't be in the too distant future".

Wednesday, July 18, 2007

The kind of shit that (not so often) happens in investment banking

So you’re leaving the office late. It’s 1am as you get into a cab to take you home. Bonus paid, money in the account and no offer at hand, so you decide to drown yourself in workaholicism, in the hope that you will forget that seven of your fellow analysts quit today and there are a good few more to come over the next few days.

You can’t believe your luck as your taxi driver dims your lights, and when you give him a puzzled look, he turns on the intercom to the passenger cabin and says:

“You looked like you wanted some peace and quiet, so I figured I’d turn down the lights so you can get a kip guv”

You thank the good man and doze off with the views of the London Eye, Buckingham Palace and other central London attractions swiftly passing beside you.

As you wake up to see the cab sitting in front of your Chelsea, flat you dig into your firm branded gym bag for your keys. And again. And again, and with more agitation at each attempt. No keys. And again. Nothing.

You must have left them at the office. Damn it. When things are going so well, here you are, having to go back to the city, get your keys and lose another hour of sleep. Damn it in deed.

You politely ask the cabbie to take you back and you try to catch a few more winks of sleep which prove to be difficult as the cabbie decides to take you Through Mayfair towards the City.

You watch the crowds of party goers outside the cab, when a familiar looking face catches your eye. You look again in disbelief, and yes, clear as daylight, it is Rupert, hailing a taxi coming in the opposite direction. With him is… Noooo! It can’t be.

“Wow!”

You think to yourself. The rumour potential of this is tremendous. It’s Rupert and Melinda, getting into a cab together. At 2 am!

Forgetting those keys in the office wasn’t so bad after all. Now this is how an hour of sleep can gain you an incredible amount of leverage. Who said that working late doesn’t have it’s benefits?

You can’t believe your luck as your taxi driver dims your lights, and when you give him a puzzled look, he turns on the intercom to the passenger cabin and says:

“You looked like you wanted some peace and quiet, so I figured I’d turn down the lights so you can get a kip guv”

You thank the good man and doze off with the views of the London Eye, Buckingham Palace and other central London attractions swiftly passing beside you.

As you wake up to see the cab sitting in front of your Chelsea, flat you dig into your firm branded gym bag for your keys. And again. And again, and with more agitation at each attempt. No keys. And again. Nothing.

You must have left them at the office. Damn it. When things are going so well, here you are, having to go back to the city, get your keys and lose another hour of sleep. Damn it in deed.

You politely ask the cabbie to take you back and you try to catch a few more winks of sleep which prove to be difficult as the cabbie decides to take you Through Mayfair towards the City.

You watch the crowds of party goers outside the cab, when a familiar looking face catches your eye. You look again in disbelief, and yes, clear as daylight, it is Rupert, hailing a taxi coming in the opposite direction. With him is… Noooo! It can’t be.

“Wow!”

You think to yourself. The rumour potential of this is tremendous. It’s Rupert and Melinda, getting into a cab together. At 2 am!

Forgetting those keys in the office wasn’t so bad after all. Now this is how an hour of sleep can gain you an incredible amount of leverage. Who said that working late doesn’t have it’s benefits?

Monday, November 06, 2006

Pearls of wisdom

You have been with the bank for almost three whole months when Rupert’s secretary comes over to your desk, asking you whether your diary is for lunch on Wednesday. Rather than replying “you should know – you’re my secretary too”, you check your diary, and notice that your diary is free all day.

You have been with the bank for almost three whole months when Rupert’s secretary comes over to your desk, asking you whether your diary is for lunch on Wednesday. Rather than replying “you should know – you’re my secretary too”, you check your diary, and notice that your diary is free all day.Like a lightning bolt, the rules of posturing flash in front of your eyes, and you reply that you don’t but if Rupert requires it, you will reschedule prior commitments to accommodate him.

It’s set. Mr. up-and-coming-on-his-way-to-becoming-a-BSD has not only mastered the art of posturing, but will also be having lunch with Rupert McMuppet on Wednesday.

The childish excitement at the fact that you have officially become Rupert’s boy makes the following two and a half days until Wednesday lunchtime sail by in an instant, and you find yourself sitting across the table from Rupert. He gives you a few minutes of bla bla on the deals you are working for him on, at which point he gets bored and decides to give you an inspiring lecture on the faux and faux pas of investment banking.

Rule No.1 – Never get too attached

You need to show commitment to win the deal. Once it’s yours, move to the next one, and make sure you don’t spend a second more than you have to working for that particular client.

Rule No.2 – The client is always right

The i-banker is not there to get things done – that’s what the lawyer does. The i-banker is not there to negotiate – that’s what management does. The i-banker is not there to think strategy – that’s what the client pays management consultant for. The i-banker is not there to provide financing – that’s what the relationship bank is there for. The i-banker is not there to provide contacts with potential acquisition targets, because the management already knows that they want to do before calling in the i-banker. So what exactly does the i-banker get paid to do? Simple – massage the client’s ego (and back up their ridiculous ideas) with 200 page presentations that only a moron would look beyond the cover page of.

Rule No.3 – Exclusivity

As per rule No.2, the banker adds a lot of value top a client. A good banker will massage so well, that a client will dread the banker being hired by their competition on a deal. As a result, the good banker will often be hired alongside another (competent) adviser, out of shear fear on the client’s part that the i-banker’s services in question may go to the competition. It is this excellence at what a banker does that has led to what is known in the industry as co-advisory (more than one –banking firm advising a single client).

Rule No.4 – Choosing the right horse

I-bankers are very much like the punters at the races. They pick horses (clients) and bet that they will win a particular deal. Just like the races, more than one punter can bet on a single horse. Unlike the races, however, if a horse wins, an i-bankers fees will not be split between the numerous i-banks advising. Each bank will get their full fee and will get league table credit for 100% of the deal value (see rule no.5).

Rule No.5 – League tables

In banking, big is always beautiful. This, however, often breaks down when it comes to fees. I-bankers will often make very little money on big deals for the sheer pleasure of being seen as the sole ass-kisser or joint ass-kisser (aka. ego masseuse). They will often make more in fees on a far smaller deal (where what they chare is much less exposed to public scrutiny, and they will need greater monetary compensation for the fact that they are not kissing ass in the limelight).

Rule No.6 –The magic is in the makeup

As you know, this forms the foundation of posturing. It is also of paramount in the work a banker does. It is a well known trade secret that i-banking is about form rather than substance and that a presentation that looks good will beat one that actually says something any day. I-banks are often asked to present themselves in a “beauty parade” – a common occurrence where a prospective client compares which bank has the best dressed bankers, the sexiest looking books and whose books make the loudest thud (the greatest amount of pages x the thickest paper and covers) when dropped on a table. The winning institution gets an advisory mandate.

Rupert decides that he has had enough of these pearls of wisdom, and asks for the bill. You wonder why people say there is no such thing as a free lunch.

Friday, November 03, 2006

The ASSociate

You know a big fat brownie has landed right in your lap when you get an email like this:

From: Moran, Seth (IBD)

Sent: 27 October 2006 16:07

To: Moncrieff, Michael (IBD)

Cc: McDermott, Mary (IBD)

Subject: Presentation for Monday

Michael,

I just spoke to Mary who said you have some capacity to help me with a short follow-on pesentation on Project Magnificent. I specifically asked for you as I know the type of work you deliver and this is one of those babies where we are so close to a deal that we cannot let it slip away from us.

As you are already familiar with the company and previous work we did for them. I have spent quite some time whilst on holiday thinking about what we need to do for Monday, and below is a list of pages I need you to create.

1.

Table of contents2.

Introduction – I will draft this.3.

Selected creds – doctor the league tables so we are No. 1 in equity, debt and M&A. I know this is hard so I don’t care how you do it. We need to be No.1.4.

Industry Snapshot – update the page we used last time with the benchmarking matrix superimposed on the attractiveness/interest matrix using a bubble chart. Try to also squeeze in there the correlation graph Charlie came up showing the relationship between size and profitability (his answer though is wrong I think) – there should be a much stronger correlation – check this and change it so that correlation is greater than 80% - I don’t care how you do it.5.

Share price graph with volume over the last 12 months, with industry and FTSE100 indexed to the start in the background, and annotated key events on the seidebars.6.

Equity research views page with price target / research house / analyst / date histogram. Also call equities and get investor sentiment feedback and put it in. Be selective here and only include positives.7.

Summary capitalization page – from share price to firm value. Also show implied EV:EBITDA multiples for 2006, 2007 and 2008. Use average IBES EBITDA estimates. Also show Implied P:Es for 2006, 2007 and 2008, again using IBES estimates.8.

Pull a list of precedent transactions and show them in a colourful bubble chart. We need the elected multiple to be about 8x LTM EBITDA, so work your way back from there when selecting which transactions to show.9.

Do a simple DCF analysis and show the implied DCF valuation. Show a page on key DCF assumptions. Run the DCF on a pre and post synergies basis. Show also the valuation difference if you use a 1% perpetuity growth or exit EBITDA approach. If it is not too much trouble, I would like to see both 5 and 10 year DCFs before deciding how to present this.10.

Run a simple LBO analysis. One page on the key assumptions. Entry multiple = exit multiple. Debt at 9x LTM EBITDA, recap after 2 years. Try to get debt pricing from capital markets before they leave for the weekend today – you may need to do this quickly as it’s 4PM already. I want to see the LBO on an OpCo:PropCo structure and a standard sale and leaseback structure, as well as the standard leveraged acquisition. It would also be interesting to see whether a REIT structure would fly for this. Don’t spend too much time on this. I don’t want you to be here

all weekend.11.

Prepare a page outlining which sponsors have invested in the industry before and hold portfolio companies in this industry.12.

Have a section on Bolton acquisitions. With the following slides:13.

Accretion / dilution analysis based on 100% cash, 75% cash, 50% cash, 25% cash and 100% stock. Show each analysis on the basis of 2005A 2006, 1007 and 2008 projected financials.14.

Illustrate the impact on the DCF of the bolt-on acquisition. In a page. Do a sensitivity table for the structure used (100% cash, 75% cash, 50% cash, 25% cash and 100% stock).15.

Do the same for the (LBO 100% cash, 75% cash, 50% cash, 25% cash and 100% stock)16.

Next section is our understanding of the business:17.

Prepare three once page case-studies based on the most appropriate precedent transactions you will find. Each case study should show analysis of strategic rationale, financial impact and iplied multiples and stock market commentary.18.

Socrecard benchmarking different options: how much debt to use, to do bolt-ons, which LBO structure to use, etc. I want moons/half moons and ticks and crosses alongside the commentary.19.

Conclusion – I will draft this.

Thanks for your help with this and call me when you have a solid draft.

Have a good weekend.

Seth

Thursday, November 02, 2006

Time = money (or so they will have you think)

Its 4AM and you are leaving the office. Your can is waiting for you outside the main entrance. You throw your firm standard gym bag into the can and hop in. You have been working 8AM and just want to sleep. After giving the driver instructions, you recline into the back seat and close your eyes. Your headache begins to ease and you begin to feel much better. You do the match in your head as you drift to sleep: you will hey half an hours sleep in the taxi, so 4:30, another thee at home which gets you to 7:30 when you need to hey up for work again. That's not bad. Thee and a half hours is more than an inten needs (you recall Ron telling you he had to make do with two when he was an inten).

Its 4AM and you are leaving the office. Your can is waiting for you outside the main entrance. You throw your firm standard gym bag into the can and hop in. You have been working 8AM and just want to sleep. After giving the driver instructions, you recline into the back seat and close your eyes. Your headache begins to ease and you begin to feel much better. You do the match in your head as you drift to sleep: you will hey half an hours sleep in the taxi, so 4:30, another thee at home which gets you to 7:30 when you need to hey up for work again. That's not bad. Thee and a half hours is more than an inten needs (you recall Ron telling you he had to make do with two when he was an inten).Your mellow train of thought is interrupted by the cab driver.

"You boys always stay up so late. How on Earth do you do it?"

Nooo. Just your luck to end up with a talker. "I do it by sleeping in the cab you dumbass, instead of talking to you! How do you think I do it ?!?" You feel like a master of the universe for a second as you picture yourself saying that to the cabbie, only to decide against it. After all, its his cab and you need to hey home. Getting thrown out would be most counterproductive in achieving that goal. You decide to ignore the driver and pretend you are asleep, hoping he will fall for it.

No such luck. He keeps on talking.

"I don't understand why you boys do these crazy hours. See, if you take my job, I work my own hours. I am my own boss. And guess what I make. Just guess. I bet you that I make more than you do and I am my own man, working less than half the hours you do."

You smile politely.

If you get one more freaking cabbie lecture you on how you shold cash in your high flyer miles and upgrade to driving sorry assholes like you around town at the most ungodly hours of the morning, you will seriously not be able to restrain yourself.

You smile politely.

You pretend to be thinking about the words he has just spoken with a newfound sobriety in an attempt to shake him off. You try as hard as you can to appear to be rejoycing in the image of your i-banker mates when you break the news to them that after three months at the firm you have chosen to leave to pursue other opportunities. Whilst you are most grateful to the exceptional individuals you have had the honour to work with, it is time for you to say adieu for you have decided to grab the bull by its horns and take your future into your own hands. The markets are booming, and it is not difficult to see that fromk the armies of bankers leaving their offices at crazy hours of the morning. You have thus decided to set up your own business and capitalise on the current market environment. Having identified a lucrative and underexploited business opportunity, you have decided to join the ranks of black cab drivers (who are far less numerous than i-bankers and thus must be far more exclusive a club). Also, judging from the crazy waiting times in the taxi ranks at the office of late, one cannot help but remark that waiting times have gotten longer and longer, and following the rules of posturing, which you have learnt so much about, it he who is more important that is waited on, so you will be taking a step up on the ladder of corporate success.

Your daydream (or nightdream - no pun intended) is interrupted by a sharp turn into Beauchamp Place. You look at the cab driver, and realise that what started as a mockery of this presumptuous chap, has turned into a real option in a matter of seconds. The fact that he can drive like a complte arse and you cannot do anything about it goes to show your respective places in the food chain. You ask him how old he is out of curiosity.

"48, going on 49 in October" he replies.

You take a look at him and he does not look a day older than 31. You then realize that the only 30-something year olds are bankers, and banker years are just like men bragging about their conquests - to get to the truth, take whatever they say and divide by 2. You do the maths in your head, taking his age 49, divide by 2 and get 24.5, and it all makes sense finally. This 49 year old cabbie is only about 24.5 i-banker years old, and he looks it!

Mental note. Add leaving email on to do list when you get back to the office.

Wednesday, November 01, 2006

Posturing - the magic is in the makeup

You know what posturing is all about. You see everyone around you do it. Rupert is an example in case, with his wide pinstripe suits, Hermes ties that scream “In your face!”, braces that he probably only wears because he saw Gordon Gecko wear them in Wall Street. The know-it-all tone and the over-chewed piping-hot-potato-in-your-mouth English accent are all part of the show. Male i-bankers can’t get away with lipstick and mascara (at least at work, anyway), but they sure can posture their way to peak of investment banking showbusiness.

You know what posturing is all about. You see everyone around you do it. Rupert is an example in case, with his wide pinstripe suits, Hermes ties that scream “In your face!”, braces that he probably only wears because he saw Gordon Gecko wear them in Wall Street. The know-it-all tone and the over-chewed piping-hot-potato-in-your-mouth English accent are all part of the show. Male i-bankers can’t get away with lipstick and mascara (at least at work, anyway), but they sure can posture their way to peak of investment banking showbusiness.10% of being a BSD (Big Swinging Dick) is knowing what you are doing. This is by no means an absolute requisite, as even if you have no clue as to what you are doing (like many BSD’s), the remaining 90% of your skill-set will kick in to overcompensate. The other 90% of being a BSD is posturing. It’s simple: if you present yourself as a BSD and keep up the show, you will be perceived to be a BSD. A simple example.

Rupert interviews you and acts like a BSD. You conclude he is a BSD. You tell your intern buddies that he’s a BSD. They tell their analysts that this Rupert guy is a major BSD (interns like to exaggerate). The analysts start telling their associates about this BSD in M&A called Rupert. The associates are always keen to get on the good side of important people (the “ass” in associate in not there by chance – it’s in fact part of the job description – kissing ass is what they do) so they go out of their way to treat Rupert (should they ever meet him) like the BSD he is rumoured to be. The VPs see everyone crawling around Rupert, and here’s where it gets interesting. Most VPs are promoted associates, and whilst you can take the ass out of the associate, you can never separate someone who’s been an associate from the ass. The rare few who question the “Rupert is a BSD” rumours and try to test this for themselves are in for a surprise. The Ruperts of the world are very well aware of the existence of these dangerous independent thinking VPs, who will usually try to come up with a smartass challenge to a point Rupert is making (usually via email, copying half the bank in an attempt to uncover the fact that Rupert is a dumbass). This will usually be done at around 6PM a day before the meeting, in an attempt to give Rupert as little time as possible to manoeuvre himself out of the situation.

This VPs, my friends, has sown the seeds for a group all-nighter, also known in the business as a clusterfuck. Rupert will have every associate, analyst and intern work through the night ion every possible combination and permutation of the pieces making up the matter at hand, to be able to see every possible scenario in the morning, before the meeting. If what the smartass VP mentioned does crop up (Scenario 1), he will staff his army of followers on finding ways of discrediting the VPs assumptions (i-bankers are very good at discrediting assumptions). If the scenario doesn’t crop up (Scenario 2), Rupert can comfortable claim that the VP does not know what he’s talking about. In either case, Rupert will reply to the VPs comment (reply to all) after the meeting and regardless of whether it’s Scenario 1 or Scenario 2 that takes place, will make the VP look like a complete muppet.

In short:

Rupert is not really a BSD.

Rupert postures as a BSD.

Rupert becomes a BSD.

Tuesday, October 31, 2006

Valuation: more art than science, more bullshit than art

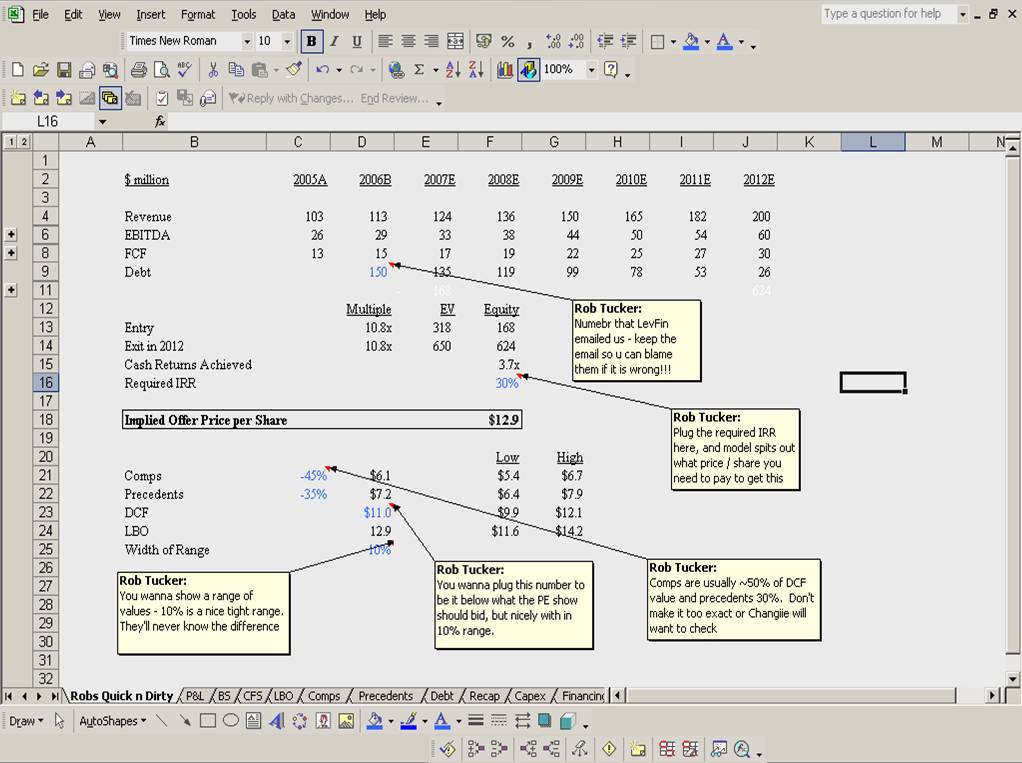

You’re manically tapping away at your keyboard, working on a valuation for Terence Chang, an MD in M&A from the New York office (alarm bells should be ringing when you hear MD, double hard when you hear M&A and off the scale when New York goes on top of that). You’re scared shitless coz everyone says that New York is the shit. They know everything and then some. They are ruthless, and they don’t give a flying fuck about the fact that you’re five hours ahead of them on this side of the pond. To make things worse, the fact that your old man is a Yank doesn’t earn you any brownie points there, unlike your English accent did with Rupert. So all you can do is tap away and give Changie the best fucking valuation he has seen in his life. No pressure!

You’re manically tapping away at your keyboard, working on a valuation for Terence Chang, an MD in M&A from the New York office (alarm bells should be ringing when you hear MD, double hard when you hear M&A and off the scale when New York goes on top of that). You’re scared shitless coz everyone says that New York is the shit. They know everything and then some. They are ruthless, and they don’t give a flying fuck about the fact that you’re five hours ahead of them on this side of the pond. To make things worse, the fact that your old man is a Yank doesn’t earn you any brownie points there, unlike your English accent did with Rupert. So all you can do is tap away and give Changie the best fucking valuation he has seen in his life. No pressure!Rob Tucker, an analyst 3 and well knows superstar of his class walks casually by your desk, stops in front of your screen, takes a quick peek and says:

“Modelling, eh? How’s it going?”

“I’m so stressed” you reply. “I’ve got to do like all the comps, precedent transactions and a full blown DCF analysis for this MD in New York M&A and then he wants me to use the valuation I get to figure out what is the lowest price his private equity client can pay and still get the deal. Shit, I’m fuckin’ stressed. I’m on my second redbull and damn. I can’t talk now. Gotta work man!”

“Chill little dude. When’s your deadline?”

“Like, tomorrow morning New York time! There is no way I can make it if I don’t work straight through the night and into tomorrow morning! Aaaargh!!!”

Rob motions for you to stand up, which you reluctantly but obediently do, and sits on your machine. He asks you to run to Starbucks and get him a black coffee and a packet of cigarettes and call him on his mobile when you’re standing outside the main entrance. Reluctantly, you go to Starbucks.

Having called Rob once in front of the entrance, you see him coming out. You give him the coffee as he motions for you to give his a cigarette. He lights up and begins walking casually. You follow, annoyed at the way this asshole is wasting your precious modelling time and making you buy him coffee and smokes, and then wastes your time while he has his coffee and smokes, when the clock is ticking on Changie’s valuation!

“Chill little dude. You’ll be fine, you’ll see.”

The smoke coming out of the corners of his mouth makes him look like a Chinese dragon as he says.

“We really shouldn’t be smoking this shit. If you knew the kind of crap they stuff into these smokes, you would never smoke again.”

Rob worked on a tobacco deal, and knew all there was to know about tobacco. He also took no shame in demonstrating this knowledge. Come to think of it, he took no shame in anything. You first got to know Rob as you were leaving the office at 3AM one morning, and a voice behind a mountain of smoke hollered.

“We don’t pay interns to sleep. It’s only thee buddy – whatever happened to face time?”

Your fellow intern buddy explained that that was Rob, the analyst he was staffed with, who let him go home early that night and offered to wrap up his share of the work. Wow! “What a nice guy – let me leave at 3!”.

Rob proceeds to give you advice on how to play office politics, with each sentence being interrupted by him saying hi to someone coming out of the building. How many people does this guy know!?!

You are torn between a sad admiration for how plugged in this kid is and the increasingly uncontrollable desire to strangle him for wasting your precious modelling time.

He finally puts out his cigarette and motions for you to follow him up.

Once you guys make it back upstairs, he sits back down on your machine, checks your email, where a you have an email from a dude in leveraged finance. You glance at the email traffic and here’s how it reads:

From: Cartwright, James (FIN)

To: Moncrieff, Michael (IBD)

Terry and Michael,

We've done the best we could at such short notice. I've had three of my guys running around like headless chickens trying to get this done, but the result is still a little rough and readfy. Still, it should be correct give or take US$5m. We think your sponsor should be able to raise US$150m for Bollocks Industries

Hope this is ok.

James

James Cartwright

Managing Director

Leveraged Finance

T: +44 20 7641 2791

F: +44 20 7641 2777

>>From: Moncrieff, Michael (IBD)

>>Sent: 31 October 2006 15:49

>>To: Cartwright, James (FIN)

>>Subject:

>>Jim,

>>

>>Chang here. My analyst needs the debt capacity for Bollocks Industries for a meeting with a >>sponsor ASAP. I'm waiting on you by his machine. I expect a number in 15.

>>

>>Terry Chang

The bastard emailed the co-head of LevFin pretending to be Terry Chang from YOUR MACHINE! Shit! You panic, wanting to beat the crap out of this arrogant shit sitting on your machine, only to realise that he’s just saved you six hours of benchmarking analysis that will anyhow be ripped to shreds in a day’s time. So what if his methods are a little unconventional, right? Shit! He can get you fired! Arrrrrgh! You don’t wanna be the dude that got fired before actually getting hired. As you continue freaking out, Rob looks back at you and calls.

“Your analysis is done little buddy. All you need to do is send this to graphics to make a few nice slides and pack your shit, coz we’re going for a few beers to celebrate.”

You look at Rob in amazement. He has finally gone mad! Pulling a prank on the LevFin co-head is one thing, but you still have midnight oil to burn on the rest of the valuation. As if he just read your thoughts, rob points to the screen and says.

“Don’t worry little buddy. It’s all done, and I’ve even made little comments for you in the spreadsheet, so you can freshen up on how we cheated Changy tomorrow morning. And now, it’s beer time.”

You take a quick look at the magic solution to your all-nighter problems that seems to have materialized on your screen, before you send it to graphics as instructed. Tomorrow morning, you’ll have the slides Changy wants way before he gets up in New York and you will rock.

You pick up your stuff and head to the pub with Rob. You begin to understand why he’s a superstar. Not because he is so much better than anyone else alive. Far from it, it’s just that he’s a tad less stupid than the rest of the crowd, and smart enough to have learnt that in i-banking, form beats substance. Every time.

Monday, October 30, 2006

Review time (you scratch my back, I’ll scratch yours)

You’ve been around for long enough to participate in the firm’s 360 degree review process. This is where people you have worked with get to review you, saying what you’re good at and what you need to improve on. The beauty of the game is that you also get to review them. HR thought up this sophisticated review system that should make sure that reviews are objective and that juniors are able to voice their opinions on the performance of their seniors. However, unlike the art of gift giving, in banking, it is not only the “thought that counts”. The 360 review process is really a large-scale exercise in the age old strategy of “you scratch my back and I’ll scratch yours”.

You’ve been around for long enough to participate in the firm’s 360 degree review process. This is where people you have worked with get to review you, saying what you’re good at and what you need to improve on. The beauty of the game is that you also get to review them. HR thought up this sophisticated review system that should make sure that reviews are objective and that juniors are able to voice their opinions on the performance of their seniors. However, unlike the art of gift giving, in banking, it is not only the “thought that counts”. The 360 review process is really a large-scale exercise in the age old strategy of “you scratch my back and I’ll scratch yours”.You have been asked to review Gianfranco, an associate you have been working with very extensively on a merger the past few weeks, who is also the most incompetent and lazy individual you have met in your life. You sit looking puzzled at the assessment form, scratching your head as to how you can come up with anything even remotely warranting a positive comment from your experience of working with Gianfranco.

“What are his key strengths (name five)? Note any areas for development:”

Key strengths? Like finding any strengths wasn’t enough of a challenge, you want me to find the key ones?!? Areas for development – p-leeeeease! You can list everything under the sun and then some and you wouldn’t even be close. Start from the fact that he cannot write (and to a large extent speak in) English if his life depended on it. He can’t do numbers (which can be a strength because he wouldn’t be able to spot a fuckup in your models ever), he dresses like a Sicilian mafioso and uses more cooking oil to slick back his greasy long hair that all the kebab shops in London do in a year. What more can you say than this individual simply sucks?!?

You look up to your screen, and hey presto, not even five minutes since HR has informed you that you and Gianfranco will be reviewing each other, you have an email from Gianfranco in your inbox.

“Ciao buddy. You wanna go an have a coffee? I buy, ok”

You reply saying sure and five minutes later, the two of you are sitting in Azzurro, the Italian café round the corner with two espressos in front of you. After no more than the bare minimum needed to vaguely resemble a polite conversation opener from Gianfranco (not that he’s being rude on purpose, but the dumb shit can’t speak any damn English), he cuts to the chase.

“So, e, I ‘a see ‘a dat ‘a you an me are ‘a gonna’ do’a the 360 degree, no?”

For a moment, you aren’t sure if he’s referring to the 360 review process or trying to proposition you! Admittedly, the greasy hair, half unbuttoned shirt, and sleazy look he constantly has about him don’t help here, but you decide to give him the benefit of the doubt on the back of the fact that he is consistently sleazy (this decision being reached with a rather hefty amount of hope that you are right on this one).

“Yeah, so, eh, ‘a I ‘a explain ‘a ‘ow ‘a this ‘a thing ‘a work, ok?”

“You ‘a want an offer, no? Ok, so, I a’ ‘elp you and ‘a write ’a you a good review, ok. So, an ‘a you, ‘a you ‘a ‘elp ‘a me too, no?”

Before you have time to catch your breath at this highly inappropriate proposition, he pre-empts an answer.

“Ok. Super – duper, e’. Allora, now ‘a we ‘a enjoy ‘de espresso. No more ‘a talk ‘a da work.”

Back at your desk, you get back to work. In no less than half an hour, you complete Gianfranco’s review and submit the following to HR.

“What are his key strengths (name five)? Note any areas for development:”

Gianfranco is an excellent banker, and an individual I have learnt a great deal from over the past few weeks. I have had the pleasure to learn from him and observe how the work he does wins the respect and confidence of clients and senior bankers alike. He is diligent and knowledgeable in the fundamentals of valuation. He strives for perfection and is an excellent communicator. His ability to clearly and concisely make complicated points understood is unrivalled and I am certain that this characteristic will make his an even better banker in the future. Whilst an individual could always be said to have an opportunity to develop, it would be most unfair to point out any areas for development in Gianfranco’s case, as he exceeds the expects in every aspect of investment banking. In everything he does, he takes on the responsibility (and delivers the results) that would be expected for a banker at VP level or above. He is a truly exemplary individual and I am proud to have the pleasure to learn from and work with him.

I used to be a nice guy – and now I’m a banker

It’s the weekend, and by some stroke of luck, you have managed to get your Sunday afternoon free. Nobody’s called you and no emails popped up on your blackberry for a full three hours (you actually called IT and got them to make sure that everything was ok with the company server and that all that important email traffic from your associate wasn’t getting clogged up somewhere between his blackberry and yours only to find that everything was a-ok). You are a free man for the evening. After making a few calls to your intern buddies, only to find out that they are stuck at the office, you sit on your couch and stare at the TV. You switch to Bloomberg out of sheer guilt – even though your presence is obviously not required at the office, you can make productive use of your time by keeping up to speed with what’s going on in the markets. No luck here either. Bloomberg is doing a show on how traders spend their bonuses. Flash cars, helicopters and lots of blingedy-bling-bling-bling.

Shit. What are you going to do? You’ve been an intern for a week and you don’t know how to productively use all this spare time. After surfing channels in search of something to stimulate your financially minded braincells, you decide that the TV is not the solution. You decide that the best way to serve the greater i-banking good is to use this time to build your network. You dial a few numbers and get a group of fellow interns to meet for a few drinks at the Eclipse on Walton Street. The dude from Lemming Brothers actually had the nerve to suggest meeting at his (upmarket) corner pub instead – a suggestion which was quickly shot down as no self respecting i-banker can be seen in a pub! Your two other buddies from Moron Stanley beat you to the gun on that one, leaving no doubt that Eclipse was the place to be seen.

You have a shower, gel back your hair in true American Psycho style, put on a crisp starched Polo shirt, beige Polo chinos, brown Church’s laceups, and a light blue Polo jumper (with a perfectly colour co-ordinated soft green polo player) and you’re good to go. You strap your Swiss Army watch to your wrist and wipe the drool off your face as you imagine the way everyone’s jaws will drop when you replace it with your very own Patek Philippe. You are ready to go. You walk outside, hail a cab for the three and a half minute journey to Eclipse and walk in to find the banker boys at a cushy table and a drink waiting for you.

There’s the Moron Stanley IB boys, the Italian from Lemming Brothers fixed income and his Lemming flatmate. The flatmate looks completely harmless. He’s wearing the standard Polo dominated outfit and thick rimmed glasses. He comes across as the rocket scientist that every graduating class has a specimen of. A truly odd species, who has traded in his chequered short sleeved shirt and calculator holster for a pair of miu miu pants, Prada loafers and a Polo shirt and jumper. Nonetheless, you can’t imagine him harming a fly. You can picture him diligently tapping at a discounted cash flow model, trying to make right the $0.0001 by which the balance sheet is of in 2015. Your image is shattered as you pick up a fragment of the conversation, where the Lemming flatmate, with steam almost coming out of his ears says ”…so then I told my associate to fuck off!”, after which he almost downs the remaining half of his Long Island Iced Tea. You slip back into your thoughts and go over what this harmless looking creature is living through. A person who could not harm a fly, flapping about how he told a superior to fuck off. One glance and you wouldn’t have imagined that he ever even had the nerve to complain about anything, and here he is shootin’ his shotgun like this was his daddy’s ranch in Texas. You realize that you are not all that different. You think about this for a second and conclude that you “used to be a nice guy, and now you are an i-banker”.

Saturday, October 28, 2006

Taking your i-banker hat off

A bit of cocky confidence and your fantastic ability to make shit smell like Chanel No.5 (see Working for Rupert McMuppet) gets you invited to pitch with Rupert to Company A, all on the back of your groundbreaking mini combo analysis. Well, actually, you did really try to do the same bit of “what would it look like if Company A tried to buy” every single one of its competitors, but nothing else worked. Ahem. Let’s be honest here, what you really mean is that every other potential acquisition was even worse! So Rupert triumphantly decides to go with the best of the lot. You’ve got the presentation all worked out, printed, bound and checked. The introduction slide sets out the agenda for the meeting, and summarises the work you have done. You proudly look at it with your newly acquired investment banker viewpoint and glance over it to make sure it all ties in, makes sense and that the firm (through yourself and Rupert as its channel) is delivering top notch advice to Company A. Ahem!! What you really mean to say, is that you check for typos.

Your slide looks something like this.

Your slide looks something like this.

For a brief moment, you step back, take your investment banking hat off and take a fresh look at the slide. You can hear the voice of your mentor saying “remember that our clients aren’t bankers and you must always put yourself in their shoes whenever you present to them. See the pitch the way they would see it.” You decide to put your client hat on and take a fresh look at the slide.

You put your i-banker hat on again and pack up the books and think you yourself: “Heh, aint no way these Company A guys are going to see through this. If they were so smart, they’d be i-bankers.”

Friday, October 27, 2006

Working for Rupert McMuppet

Ok. It's your first week on the job and it so totally rocks. You get to hang out with some of the best people in the industry, and the firm is so good, that they make these good times last well into the night! On your first day, you went home at 2AM, and there plenty of investment banking megabrains that enjoyed each other’s company so much, that they stayed even longer! Not only do you hang out with such fantastic people, who shape the face of the financial markets with what they do on a daily basis, but the firm also provides you with free food each night, to make this fun filled time even more pleasurable. At 7PM on the first night, your whole floor gets together and you order some Chinese takeaway. WoW! And the whole office sits around a few desks, from Analyst to Director and has deeply profound conversations about the business, colleagues, competitors and the like. How much does this rock! They're all sitting around talking about the financial markets, with you, a day into the job intern, being part to conversations loaded with so much confidential information! How lucky are you to be an investment banker. One of the junior bankers (an analyst 2, how cool) attempts to give you some advice. After telling you how to do this and not to do that, he stresses that by no means should you willingly get in the way of Rupert McMuppet! "Whatever you do, if you see him down the hall, go to the water cooler. If you see him coming to your desk, hide under it. You do not, by any means, want to work for Rupert McMuppet. You just don't!" You cannot understand what he's on about. Rupert is a great guy. He interviewed you. Granted, a bit strange, quirky dress sense, funny accent and all that but a decent guy no? You dismiss the advice whilst politely nodding. What the hell does this doochebag know. He's only a 2nd year. He's not gonna last. If he doesn't like Rupert, he wasn't made to be a master of the universe. You go back to your cubicle, a 2x2 metre box in a remote corner of the floor, where you pick up your mini combo analysis that Rupert actually asked you to do. hehe. If that muppet 2nd year knew that you were already Rupert's boy he'd eat his heart out. "Eat my dust sucker". The mini combo aint looking good. Earlier in the day, your mentor explained to you that the mini combo is one of an i-banker's best friends. It's a banker's way of justifying anything to the nmanagement of a company who are meant to protect the interests of its shareholders. The particular combo you are doing, shows that if Company A (Rupert is advising company A) buys Company B, the shareholders of Company A are worse off. That is, the'ye better off just sitting on Company A. The beauty of the mini combo is, thought, that even though a deal is shit, you can make it look good, by using debt to pay for the company you buy. Yes, you guessed it - OTM. Other People's Money! It's like if you wanna buy your 107th Hermes tie (the new one with the little clouds that are nothing like anything they have come up with before), but you don't wanna cough up the £80. See, bad deal. But if an i-banker comes up to you and says "look dude, you just cough up £20, and get payday loans for the remaining £60" it's a lot sweeter. Except, it's even better than that. When you're the management of the company, it's not you who gets into debt, it's the company. So, if things turn to shit, you bail and they lose. If all works out, you're the hero. See? It's a win, win situation. that’s what i-banking is all about. The only problem with the mini combo you're doing, is that Company A (Rupert's client) is like 20 times smaller than Company B, and no matter how much freaking debt you use, the fuckin' thing won't work. Shit! You can't go back to Rupert and tell him his idea sucks! He’s an MD and a BSD! He's the man and he thinks it rocks. You've gotta make it work man, make it work. What if you don't pay any fees for the deal. Ok, yeah, that makes it better. And, and what if your debt is really cheap, yeah, yeah better as well. And what if the price you offer for Company B is a lowball, aha, this is getting there. Aha, and what if you can get some funky accountants to help you pay less tax, aha, there you go, this baby is starting to fly. Aha, and then what if your company's earnings are say 10% higher each year. Wow, this really works now. You are the man! Rupert is gonna love this. You've just shown that his deal is a slam dunk if you can avoid tax, pay nothing for acquiring Company B, double your earnings at no cost, pay no interest and fund all of the acquisition with debt. Its 2AM and time to go home. It feels good to be in the driving seat of the financial world.

{kind=link}